This article will give you a brief idea about Input Tax Apportionment in UAE VAT Laws.

Entitlement to Recover Input Tax

Taxable individuals are entitled to reclaim input tax on goods and services, provided they meet certain criteria. This entitlement allows for the recovery of input tax in the following scenarios:

- Creating Taxable Supplies: For example, a bookstore that buys books from a supplier and sells them to customers, charging VAT on these sales, is eligible to reclaim the VAT paid to the supplier.

- Supplies Outside the UAE Taxable Within: A UAE-based company offering consulting services to a client in Egypt can reclaim the input tax if such services would be taxable within the UAE.

- Exempt Financial Services Provided Abroad: A UAE bank issuing loans to non-residents can recover the input tax, even though the service is exempt within the UAE, provided the service is considered to occur outside the UAE.

Full recovery of input tax is permissible when goods and services are used for the above purposes. However, no recovery is possible if used solely for personal consumption or to make exempt supplies, such as a private car for commuting. When goods or services support both taxable and non-taxable activities, like a mobile phone for business and personal calls, businesses must calculate the recoverable input tax for the business-use portion.

Input Tax Apportionment for a Tax Period

Businesses must apportion “residual input tax” when they incur input tax on goods or services used for both recoverable and non-recoverable activities. The process involves:

Step 1: Direct Attribution Identify the residual input tax by excluding fully recoverable or non-recoverable input tax. For each tax period:

- Ascertain the total input tax directly associated with fully recoverable supplies.

- Ascertain the total input tax directly associated with non-recoverable supplies.

- Omit any input tax explicitly disallowed under relevant regulations.

Step 2: Residual Input Tax The residual input tax includes any input tax not directly attributable to fully recoverable or non-recoverable supplies.

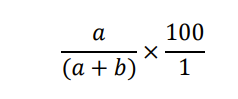

Step 3: Apportionment Percentage Calculate the apportionment rate for the residual input tax using the formula:

Apportionment Percentage = (a / (a+b)) * 100

Where:

- (a) = Wholly recoverable input tax

- (b) = Wholly non-recoverable input tax Round the percentage to the nearest whole number.

Step 4: Recoverable Input Tax Determine the recoverable portion of the residual input tax by multiplying its total by the apportionment percentage. Add this to the fully recoverable input tax to find the total recoverable input tax for the tax period.

For instance, a company with $10,000 in input tax, where $6,000 is attributable to recoverable supplies and $4,000 to non-recoverable supplies, has a residual input tax of $2,000. The apportionment percentage is 60%, making the recoverable input tax $1,200. Thus, the total recoverable input tax for the period is $7,200.

Annual Input Tax Apportionment Adjustments

Businesses must execute two essential calculations at the end of their tax year, which might not coincide with the calendar or financial year. They may synchronize these dates upon request.

Annual Washup Calculation This calculation confirms that input tax recovery corresponds with the actual usage throughout the tax year.

- Step 1: Combine Recovered Input Tax Sum the input tax claimed on tax returns during the tax year.

- Step 2: Recalculate Recoverable Input Tax Consider the entire tax year as a single tax period and recalculate the recoverable input tax using direct attribution and residual input tax principles.

- Step 3: Calculate Annual Washup Adjustment Deduct the total recoverable input tax from Step 1 from the recalculated amount in Step 2 to determine any necessary adjustment.

For example, a company’s tax year concludes in December. They claimed $50,000 in input tax during the year. At year-end, the recalculated recoverable input tax amounts to $52,000, necessitating a $2,000 adjustment in input tax recovery.

Actual Use Adjustment Post-annual washup, businesses adjust input tax recovery based on the actual use of goods and services over the year, potentially leading to further recovery or repayment of input tax.

For instance, a company discovers that they did not use a portion of services for taxable supplies, for which they had recovered input tax. They must repay the input tax corresponding to the actual non-taxable use.

These annual adjustments ensure accurate reflection of the business’s activities and compliance with tax regulations. Consult ProAct or the relevant tax authority for specific details about Input Tax Apportionment as per UAE VAT Laws.

Alternative Input Tax Apportionment Methods

The Federal Tax Authority (FTA) allows businesses to apply for alternative methods that more accurately represent their actual use of goods and services. Approved methods take effect from the next tax period’s start.

Alternative Input Tax Apportionment Methods allowed by FTA are,

- Outputs-Based Method: Apportion input tax based on the ratio of taxable outputs to total outputs.

- Transaction Count Method: Allocate input tax according to the number of taxable transactions relative to total transactions.

- Floorspace Method: Use the ratio of floorspace dedicated to taxable activities versus total floorspace for apportioning input tax.

- Sectoral Method: For businesses with distinct sectors, apportion input tax based on each sector’s usage.

These methods aim for a fairer representation of economic activity and VAT-related goods and services usage. Maintain detailed records to support the chosen method and be prepared to justify the selection to the FTA. Always verify specific details and eligibility with local tax laws.

Outputs-Based Method

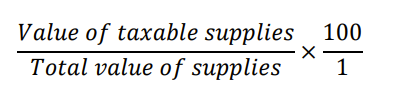

This method determines the apportionment percentage by comparing the value of taxable supplies to the total supplies made by the business. The formula is:

Recovery Ratio= (Value of Taxable Supplies / Total Value of Supplies) * 100

It suits businesses with a direct correlation between VAT incurred and income.

Eligibility: Sectors eligible for the outputs-based method include:

- Insurance companies (Islamic and non-Islamic)

- Financial institutions providing banking services

- Local passenger transportation services

- Educational institutions

- Non-business entities like art galleries

Transaction Count Method

This method calculates the apportionment percentage using the ratio of taxable transactions to total transactions. The formula is:

Apportionment Percentage= (Number of Taxable Transactions / Total Number of Transactions) * 100

It’s ideal when VAT on expenses aligns more with transaction count than income value.

Eligibility: The transaction count method fits financial institutions with transactions distinctly classified as wholly taxable or exempt.

Floorspace Method

This method uses the ratio of floorspace for taxable activities to total floorspace to calculate the apportionment percentage. The formula is:

Apportionment Percentage= (Floor Space for making taxable supplies / Total Floor Space) * 100

It’s appropriate for businesses like landlords and real estate companies with designated areas for taxable or non-taxable activities.

Sectoral Method

Large businesses with distinct divisions may opt for the sectoral method, which involves:

- Identifying residual input tax per general rules.

- Allocating residual input tax related to a sector to that sector.

- Dividing the remaining residual input tax among sectors.

- Assigning a specific input tax apportionment method to each sector.

This method aligns VAT recovery with the economic activity of each division, useful for complex businesses like banks or insurance companies with diverse operations.

For businesses with multiple sectors, it’s necessary to allocate the input tax accordingly. Two methods are:

- Headcount Method: Based on the FTE count in each sector, using the formula:

Apportionment Percentage= (Number of FTE Members in the Relevant Sector / Total Number of FTE) *100

For instance, an insurance company with 100 FTEs, 40 in life insurance, would allocate 40% of the residual input tax to the life insurance sector.

2. Outputs Method This method assigns input tax based on each sector’s income, mirroring the relationship between expenses and revenue.

Formula: The apportionment percentage is calculated as:

Apportionment Percentage= (Value of Sector’s Supplies / Total Value of Supplies) * 100

Example: If a company’s total supplies are worth $1 million, and the retail division contributes $300,000, then the retail division receives 30% of the residual input tax.

Applicability: The outputs method fits large, multifaceted organizations with clear divisions. This includes banks with distinct retail and investment branches, insurance companies offering various insurance products, and real estate firms overseeing commercial and residential properties. The method selection hinges on the business nature and the most accurate attribution of direct costs.

Consult ProAct or the relevant tax authority for specific details about Input Tax Apportionment as per UAE VAT Laws.

Contact ProAct for more information.

ProAct Chartered Accountants, a prominent Auditing and Accounting firm in the UAE, delivers personalized and top-tier services to a diverse clientele across the country. Our exceptional team of accountants, auditors, and tax consultants ensures that we meet the unique needs and demands of our clients.